[ad_1]

The derivatives market has deepened considerably, with institutional and retail investor participation in futures and options surging in recent years.

Mutual funds often use derivatives for hedging. Some categories of schemes also use safe strategies with futures and options to derive steady returns.

Among the key mutual fund categories that use derivatives extensively are equity savings, arbitrage and balanced advantage funds.

These arbitrage funds are almost entirely focused on deriving returns by using derivatives. In particular, they look to gain from the price differentials in the cash and derivatives markets. Many such funds have been around for a while now. Though returns are moderate and more in line with those of debt schemes, arbitrage funds score on the taxation front.

In this regard, Bajaj Finserv has created a new arbitrage fund. The NFO is open till September 13. Read on for more on the arbitrage category and to take a call on whether you should invest in the new fund.

How arbitrage funds work

This popular strategy used by mutual funds involves buying a share in the cash market. The fund manager would also short (sell) the same company’s stock in the futures market if it trades at a higher price than in the cash market. For example, a stock trades at Rs 100 in the cash market and Rs 105 in the futures market. The fund manager will buy in the cash market and sell in the futures market. During the expiry of the derivatives contract, three scenarios could emerge.

If the stock remains at Rs 100, then the investor will gain Rs 5 per share from the sale in the futures market. In case the stock moves to Rs 110, there will be a Rs 5 loss in the futures market (110-105), but Rs 10 gain in the cash market (110-100), resulting in a net gain of Rs 5 per share. Consider a scenario when the share price falls to Rs 90. The loss in the cash market would be Rs 10 (100-90). But the gains in the futures market would be Rs 15 (105-90), resulting in a net gain of Rs 5.

Thus, the fund manager makes a fixed gain in all three scenarios. We do not consider the brokerage, STT and other costs for the sake of simplicity.

Sometimes, the buying and selling can precede the derivative expiry date if there is a chance for better profits. Positions can also be rolled over to the subsequent month if the market movements are favourable.

The fund manager’s profit with the strategy acts as an accrual income for the fund.

For most parts, this spot-futures arbitrage is fairly low on risk. It can be replicated with indices as well.

Of course, arbitrage availability is dependent on traded volumes, market conditions, participation of foreign institutional investors and so on.

What should investors do?

In general, for retail investors, arbitrage funds deliver just about debt-like returns over the medium or even longer term. In the best of times, they could deliver a percentage point or more than liquid funds or just about match a few other debt fund categories. Over the longer term, expecting a f 6-7 per cent return may be more par for the course. Of course, there is no certainty about this happening consistently, and there may be periods of very low and even negative returns as well.

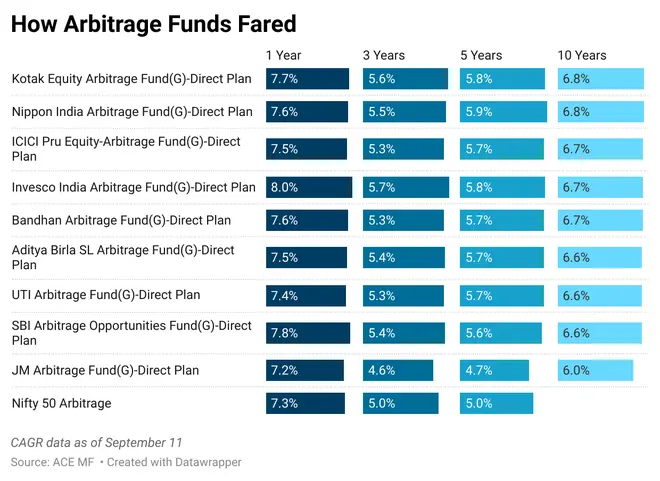

Most of the arbitrage funds have delivered more than 7 per cent in the last one year. But over longer timeframes, the returns haven’t been as high.

But the real advantage that arbitrage funds have is the equity taxation they enjoy. So, long-term gains made beyond a holding period of 12 months are taxed at 10 per cent beyond Rs 1 lakh. Short-term gains are taxed at 15 per cent. Debt fund gains are added to your income and taxed at the applicable slab, irrespective of holding periods.

An arbitrage fund’s role in a retail investor’s portfolio is limited. It can be a small part of an investor’s satellite portfolio as a diversifier.

Kotak Equity Arbitrage and Nippon India Arbitrage are two funds that have a fairly healthy track record.

Investors can wait for new asset management company Bajaj Finserv’s Arbitrage Fund to develop a track record.

[ad_2]

Source link