[ad_1]

Sovereign Gold Bond (SGB) is losing shine, as a collection through these bonds saw a dip of around 46 per cent during fiscal year 2022-23 compared to the fiscal year 2021-22. Interestingly, the return on investment was in double digit.

Multiple reasons include no correction in prices and consequent higher issue prices. Issue prices for ten tranches during F 22 ranged between ₹4,777-5,109 a gram. However, in FY23, prices for four tranches ranged between ₹5,041-5,611. Interestingly, India‘s gold imports fell by 24.15% to $35bn in 2022-23 due to global economic uncertainty and a high import duty on gold.

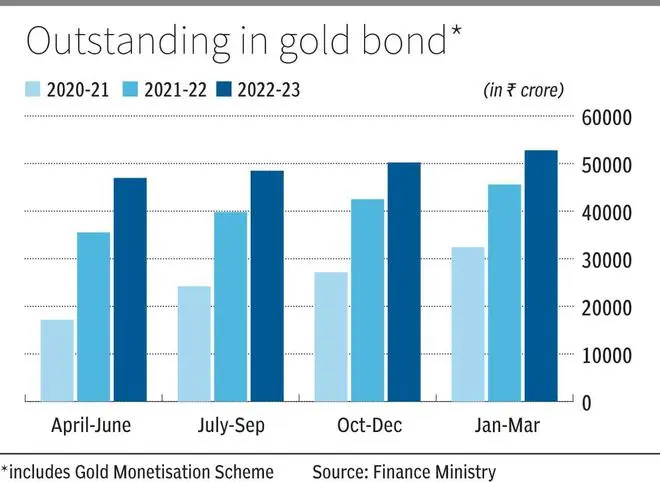

Data on government borrowing data complied by Finance Ministry, total collection through SGB (including the gold monetisation scheme) was over ₹7,100 crore in FY23 as compared to over ₹13,100 crore in FY22. Collection through SGB is part of overall government borrowing. Quarterly data of overall borrowing is placed in the public domain after a lag of three months which means data up to March 31 will be placed during the last week of June.

Vandana Bharti, Head of Commodity Research with SMC, says normally, gold sees a correction from July-September quarter, but during FY23 it did not happen. At the same time, the equity market defied the fear of recession and continued rising, which positively impacted mutual funds. “As SGB is 8 year scheme, so people would prefer to go for shorter duration investment option and they are finding that in equity and mutual fund,” she said.

According to RBI, SGBs are government securities denominated in grams of gold. They are substitutes for holding physical gold. Investors have to pay the issue price in cash, and the bonds will be redeemed in cash on maturity. The Bond is issued by Reserve Bank on behalf of Government of India.

Despite lower collection, experts still feel SGB is a better option considering principal and interest backed by the government, which means doing away with the risk of default, so they advise parking one part of total resources. Naveen Mathur, Director (Commodities and Currencies) with Anand Rathi Shares and Stock Brokers, says SGBs mirror the price of gold as gold ETFs do. Still, they cab pay 2.5 per cent annual interest on the principal amount. Above all, it is a great investment to diversify the portfolio’s risk.

“In present times where global economies are facing considerable risk of slowdown in upcoming years in times of higher interest rates, Gold is often viewed as an effective investment instrument to diversify one’s portfolio risk, where at least 10 – 15 per cent of total investment allocation should be considered for a time horizon of 5 – 8 years,” he said.

Bharti felt that though 2.5 per cent interest, calculated at issue price, on SGB is icing on the cake; it will be more attractive once the overall interest rate sees a downward trend. She advises keeping 5 per cent of total resources for investment in SGB.

For the first half of the current fiscal year, the government, in consultation with RBI, has lined up two tranches, of which first one closed early this week with an issue price of ₹5,926, per gram.

[ad_2]

Source link